How I Invest 📈 | My current investments, asset allocation, & favorite learning resources

A peek inside my portfolio...

Hey there. 👋 The newsletter looks different right? I’ve transitioned my Money Monday newsletter from MailChimp to Substack. It’s been a minute so thanks for sticking with me. COVID-19 and a closed preschool have changed how I’ve allocated my time these past few months. Caring for our little guy and trying to be professionally productive are often at odds. I hope to get in a better rhythm and hope you like the new format.

In today’s newsletter I want to share a simple overview of how I think about investing and building wealth.

I’ll share a peek behind the curtain: what I’m invested in, my asset allocation, and more.

But first, for any new readers that don’t know me, a brief introduction:

Who Are You?

👨💼 Ex-Cube Dweller: I’m a former CPA that worked in accounting and corporate finance for a number of years at places like Deloitte, PepsiCo, & General Mills.

💻 Business Starter: Corporate life left me feeling empty. And on top if that, it didn’t result in much wealth creation. I was thoroughly freaked out that my next 20 working years would be the same as the first 10 and decided the best odds for an escape was to start a business. I started small and put one foot in front of the other.

🛒 Business Seller: Long story short, my business grew from an initial $5k to a seven-figure business which I eventually sold. It was a life-changing blessing. You can hear the podcast version of my story on the My First Million podcast here.

👪 Investor/Consultant/Parent/Human: Now I spend my time parenting an amazing little person, doing e-com consulting for brands that want to get big on Amazon, and investing. I have a considerable amount of freedom which is all I ever wanted. I’ve always been a stock market junkie and investing nerd so it’s been fun to have the time and resources to focus on this hobby.

How Do I Invest? 📈

I’ve never had a financial advisor (too much of a DIY control freak for that) but if I did my first question would be “what are you invested in, why, and how has it performed relative to the market?”. Spare me the hard sell and glossy handouts… just give me the cold hard facts!

So likewise, if you’re going to read my writing where I opine on a variety of money/investing/market topics, I suppose it’s only fair I share how I invest. Selfishly this serves as a way for me to get more clarity on my own thinking, philosophy, and strategy.

I was listening to a great video featuring Gavin Baker the other day. He said a lot of things that stuck in my mind (you can read my summary via this thread) but my favorite was about the search for truth.

Investing, much like life, is all about searching for truth. It’s balancing conviction and flexibility. And as Gavin went on to say, humility and flexibly are key ingredients to being a good investor. That probably applies to being good at life as well. Stay humble. Stay flexible.

This newsletter series is my search for truth so thanks for joining me on the ride.

Disclaimer: I am not a professional trader/advisor and nothing in this issue or future issues should construed as investment advice! Factors like age, risk tolerance, preservation vs accumulation, financial goals, and more can have a big impact on how one might allocate their hard-earned personal capital. Know thyself and do your own work :-)

Lets Talk $$$ + Our Asset Allocation

Should we be more open about money?

People talk a lot about money but they never really spill the beans and truly talk about money. For a variety of reasons talking about money is a taboo subject. I’m not ready to advocate that we all reveal each and every detail of our financial lives but a little detachment from money and open sharing might be healthy. We can learn, grow, and hopefully find some truth.

I suspect most of us are seeking the same things: security for our family, freedom to live life on our own terms, and to realize our version of purpose, happiness, and contentment. Money is just the means to reach our desired ends.

Educating ourselves and our children about both the fundamental principles and psychological aspects of money and investing can do a lot of good. I learn best when it’s active learning. Listening, sharing, collaborating, and evolving my thinking. Money matters are often so guarded and that can be to the detriment of learning. So here’s my attempt at being a bit more open in hopes we both learn something from it.

Thanks for allowing that preamble! With that, lets talk about money.

Asset Allocation - May 2020

One of the most important decisions a business will make is how they allocate their capital. A family or a person is, in essence, a micro-business entity with revenue, expenses, and balance sheet. It’s equally true that one of the most important decisions to be made is how to allocate your personal or family capital.

Without context it’s impossible to have a strong opinion on if an asset allocation is appropriate. Goals, age, risk tolerance, and a host of other factors impact allocation decisions. Context, nuance, and the ‘why’ matter a lot when it comes to allocation.

I’ll share additional thoughts on our ‘why’ but first here’s the breakdown of how our personal capital is allocated (the “% of Total” column” versus what I’m targeting (“Target Allocation” column):

Pie Chart of Investments:

Thoughts on Asset Allocation

Until my mid-30’s I never bothered to track asset allocation. I was just trying to earn a bit of money, pay the bills, and hopefully watch my 401k grow. After selling a business and having a kid I realized it was probably smart to become more thoughtful about our finances. If you’re single and childless in your 20’s you can recover from big swings and misses personally/professionally/financially. Your 30’s with a kid feels a lot different (for me at least). If you don’t have a simple Google doc where you track you asset allocation I’d recommend creating one. It’s well-worth measuring.

Today I’m feeling a push/pull tension between safety and growth. When the market got smoked in March I was happy to have a relatively sizable allocation to cash. But now that the market has shot up I’m feeling regret that I didn’t deploy more of that cash into the market. You know logically you have to take risk to generate returns but risk sure can feel pretty uncomfortable in the midst of a big draw-down.

My goal or ‘why’ with our allocation is to have a mix of growth and preservation. The stocks will hopefully provide growth while the cash & bonds (and to some extent the RE) provide more stability and security.

At the end of the day my feeling is that we all have to find an asset allocation that allows us to sleep at night. March wasn’t fun but I was never laying in bed in a cold sweat. I suppose this means our asset allocation is at least somewhere close to where it should be.

PORTFOLIO BREAKDOWN

Now that I’ve shared our allocation to each asset, I’m going to further break-down the components of each one and the role they play. What is inside the stocks allocation and why? How do you invest in real estate and why?

STOCKS

It’s crazy you can click a button and own a slice of a company. That’s just mind-blowingly insane when you think about it. And even wilder, with a click of a button you can own a slice of 500+ companies.

Stocks will be my top allocation for a long time. If you’re long human progress, technology, and innovation, then I think it stands to reason you want to own businesses that participate in that progress and ever increasing economic development.

When it comes to stock ownership I’m partial to passive management. The smartest people in the world have trouble consistently beating the market over time. Not only that, there are fees and tax disadvantages of active management. So the majority of our stocks are in Vanguard index funds (VTI and VXUS to be specific).

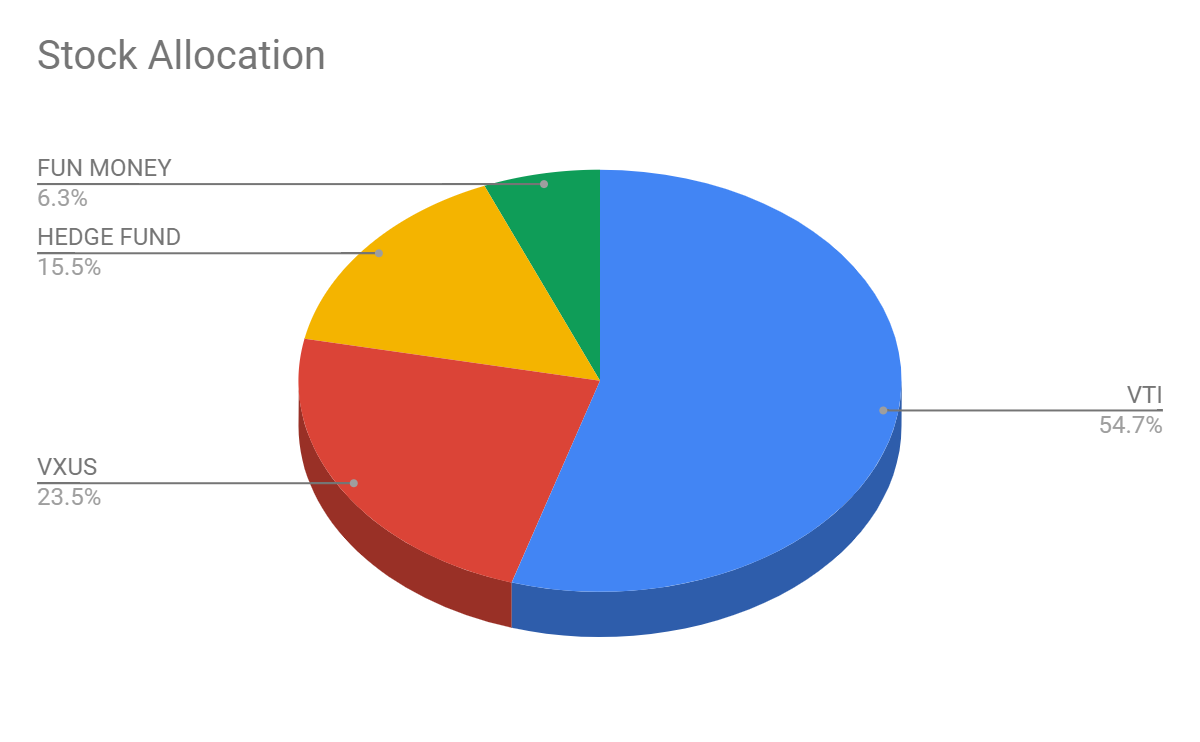

Here is the breakdown of our stocks bucket with more commentary after the chart.

May 2020 Stock Allocation By Type

Our Stock Allocation

INDEX FUNDS = 75%+: Set it and forget. Chances are you’ll beat the smart money. Why index funds? Minimal fees. Max liquidity. Market returns. I expect index funds to always be my top allocation bucket within stocks. We’re 70/30 between VTI and VXUS which is a US index fund and an international index fund respectively.

ACTIVE MANAGEMENT = ~15%: I surprised myself in choosing to become a LP in an actively managed hedge fund. Why did I do it? Two reasons: 1) Edge. I believe the fund manager has a true ‘edge’ that will allow him to generate alpha 2) Diversification. The fund is focused on small caps. Increasingly, index funds are driven by a relatively small number of stocks (Amazon, Microsoft, Google, FB, etc). Having a manager sifting though great businesses in the small and microcap space felt like a good diversifyer from indexing.

FUN MONEY = <10%: Much of my senior year at UW Madison was spent playing poker. Was this the best ROI of my time and energy? Probably not but it sure was a lot of fun. Picking stocks is the same sort of dopamine hit for me. Index fund investing might be prudent but it is especially exciting or fun? Nah. It’s boring which is kinda the point. So enter my Fun Money portfolio where I pick stocks. In March of this year I broke down and started buying individual names again. But I made a rule… no more than 10% goes to the fun money portfolio. So far I’m beating Mr. Market which is probably the worst thing that could have happened to me in the long run due to my newfound overconfidence in picking winners.

FUN MONEY CAPITAL PARTNERS, LLP 🤑

As mentioned, in March the siren song of stock picking just got too strong. I do my research and hope to choose winners but either way I can’t blow myself up with a 10% allocation.

Here are my stock picks and results thus far:

I went heavy tech in March and it has paid off as tech has roared back. As a counterbalance I have added some non-tech names like Berkshire, Altria, and Wells Fargo. Those have been slow to bounce back but I believe are strong holdings over the long-term. I intend to hold most positions for at least a year and more likely five years or longer.

Researching these companies and making investments has been incredibly fun. I plan do more and more of this as process results in good learnings and thoroughly enjoy it.

How do I pick which stocks to invest in?

The underlying principle is that I copy smart people. How? I primarily do three things:

Looking at the 13F of great managers on Whale Wisdom (e.g. I mentioned I respected Gavin Baker’s thinking before… here is his fund’s 13F from 3/31). I’ll look for patterns, themes, or commonly held names.

Listening to a lot of podcasts (mentioned below) and hearing opinions on names, trends, industries, etc

Scouring Twitter and getting ideas and thesis’s from smart investors

I let all that info bounce around in my head, write down my ideas in a spreadsheet, and then act accordingly. When the draw-down hit in March I already had a lot of comfort in the video game stocks, FB, TWLO, and the other names. So while it wasn’t especially comfortable buying into a nose-diving market, I had strong conviction in a couple years those names would be up significantly. These are great businesses with macro-tailwinds that will continue to print money for years and years to come.

I’ll share my names on my watch-list, new adds, and more in future updates.

Note: share price data as of 5/25/20

REAL ESTATE

We have a sizable allocation to real estate. Why?

Why real estate?

Diversification: Real estate certainly isn’t an uncorrelated asset but it does provide diversification from stock investments

Tax advantages: There are some tax advantages to owning real estate. Opportunity zone real estate investments made sense for me given I sold a business and incurred capital gains. I don’t know if the legislation is good public policy but if you have cap gains it’s worth checking out as it’s a once-in-a-lifetime type of program that allows for tax free gains.

Income + Growth: Good real estate can throw off healthy cash flow similar to a bond. That income each quarter will help to cover our expenses. Additionally, over time good real estate tends to rise in value and result in appreciation. So I like the mix of current income plus long term growth and preservation that real estate provides.

When it comes to real estate there are a variety of choices on the menu:

Multi-Family

Single Family

Office

Retail

Industrial

Workforce Housing

Student Housing

Self-Storage

Manufactured Housing (Mobile Homes)

My RE Investments

I’m an LP in a few different real estate funds. The investments are primarily multi-family with a little bit of manufactured housing.

Each fund I’m in has 7+ properties inside it. So 4 funds x 7 properties per fund = 28 assets I have a small slice of. They’re all US based and in cities like Charlotte, Houston, Nashville, Charleston, and LA. It helps me sleep at night knowing there is a lot of geographic and manager diversification versus having the entire allocation in a small handful of properties and markets.

Why multi-family and manufactured housing? To me, those are the lowest risk areas of real estate. We all need somewhere to live.

Office will likely have lasting challenges with the rise of remote work (although I tend to think the doomsday predictions about the destruction of office are overdone). Retail faces a continued headwind of ecommerce. Student housing will likely change as our education system changes and second tier universities go bust. Each class of real estate is facing it’s own set of challenges due to the virus and it’s knock on effects. Like the stock market, there is nowhere risk-free to hide!

Multifamily clearly has risk too, especially if enough people change their preference from urban living to suburban or rural. But net net I think multi-family is one of the safest places in real estate to put capital.

Why not just buy my own real estate?

I’m not handy. Each generation loses something I guess. My grandfather could fix anything. He worked on airplanes in WW2 and owned his own service station where he repaired cars. Growing up (and to this day) I’m in awe of the life he lived and the real skills he had. My dad is very handy as well. I am not handy. Basic fixes require watching a YouTube video countless times and still have a low success rate. All of this is to say managing a rental property and doing little fixes just isn’t a competence for me.

I’m lazy. I really don’t want to fuss with managing tenets, collecting rent, calling contractors, etc.

Being a passive LP and letting someone else manage the real estate works best for me.

Smart person to check out: Moses Kagan - If you’re looking to learn more about real estate search for Moses’ podcasts appearances and give him a follow on Twitter. He articulates the concepts of RE clearly and is a straight shooter.

CASH

“Cash is king” Unknown Attribution

“Cash is trash” Ray Dalio on 1/21/20

So which is it? Is cash king or is cash trash?

Both are true in their own way. For a family experiencing a job loss, cash most certainly is king right now. Same thing for a small business. If you have zero revenue and only a month of cash the outlook isn’t pretty. When you need it, cash is everything.

The other side of the coin (bill?) is that cash is a depreciating asset. Each and every year it loses ~2% of it’s value. If we allocated all our personal capital to cash we’d experience a slow decay in our purchasing power. Take that out long enough and one’s wealth is greatly diminished.

So there’s a cash dance we all have to do… have enough to get us through but not so much that it drags our wealth down.

BONDS

I largely view bonds in the same light as cash (especially in today’s low interest rate world). They’re safety asset. If the market has a major draw down I can convert bonds to equities. Given monetary policy and the low interest rate environment we have a lower allocation here than you might see some experts historically recommend.

We have most all our bond holdings in one Vanguard fund (BND).

PRIVATE EQUITY | VENTURE

I recently signed docs for my first private company investment. More to share down the road on that.

Why am I considering investing in a PE fund or venture? The thought process is largely the same as the reason to invest in stocks. It’s compelling to own good businesses that generate cash over a long time horizon. Start-ups and many small business obviously don’t have as clear of line of sight to becoming ‘good’ businesses but if they do the returns can be out-sized.

My goal here is not only to generate returns but also learn. When you’re an LP you get access to smart people and see behind the curtain of how businesses work. It can allow you to become a smarter investor or operator, grow your network, and inspire new business ideas you might not otherwise thought about.

CRYPTO

As Chamath says, BTC is schmuck insurance. I agree with the sentiment and have 1% of our portfolio in crypto. I’ve read a lot of about BTC and get the thesis but I’m not an expert in monetary policy or blockchain/crypto at large.

My reasoning (for better or worse) is largely that a lot of people much smarter than I have a some level of allocation to crypto. So I think it makes sense to allocate 1%. If BTC goes to zero it won’t change my life. And in the chance BTC realizes it’s potential I’ll participate and won’t be on the sidelines.

My Favorite Investing Resources 📚

Twitter - probably THE best place to learn about investing and to get stock ideas. There are loads of smart investors on the platform. A few of my favs are Gavin Baker, Dan McMurtrie, and Ben Carlson.

Pro tip: I enjoy looking at the ‘likes’ of smart people on Twitter to see what thoughts and ideas are resonating with them. To find new people to follow I’ll look at who they are following, sample the feed, and follow those that seem interesting.

Podcasts - Invest Like The Best is an absolute must listen. I also enjoy the Meb Faber Show, Capital Allocators, The Acquirers Podcast, and Venture Stories.

Bogleheads - A great forum of primarily passive (index fund) investors. Whenever I’m searching for almost any personal finance of investing topic I’ll add ‘bogleheads’ at the end of my search. E.g. “Life insurance bogleheads”, “car insurance bogleheads”, etc. A lot of practical investing and personal finance learning can be done here.

Alt Investment Club - Coming December 2020… I’m building a community of investors to help discover, diligence, and access alternative investment deals (e.g. real estate, venture capital, micro PE). If that sounds interesting to you apply for free membership at altinvestmentclub.com.

Thanks for reading!

-Paul

👋 Say hi on Twitter

🎧 In my headphones now: “I See You” | Phoebe Bridgers

📧 Help me grow by clicking the green button below and sharing. Thanks 🙏

Paul when you write that you are an LP in real estate funds do you mean PE or funds on the stock exchange?